The best contributors during the month were Fortnox, ICICI Bank, and HCA Healthcare. Those that showed the weakest contribution during March were ASM, Saint-Gobain, and Atlas Copco. Generally speaking, the stocks that have not been affected by the ongoing political debacle in the US performed well, while cyclical stocks for which there is a risk that the spectacle can impact underlying demand and earnings growth had a more challenging month. Fortnox—the portfolio holding providing the best contribution to the fund's performance in March—was the subject of a takeover bid on the last day of the month, when the company's largest owner, Olof Hallrup, together with EQT submitted a bid at a some 40% premium to the previous trading day's closing price. We own almost 1% of Fortnox and it does sting to have to say goodbye to the company, which is the epitome of a Champion, with its dominant position in a niche market, robust pricing power, high customer growth, scalable cost base, stellar cash conversion, solid balance sheet, and more. Of course, freeing up some cash in these turbulent times is a comfort, and we can invest this in other holdings that we find to be trading at appealing valuations

Key market events and trends (what has influenced performance most?)

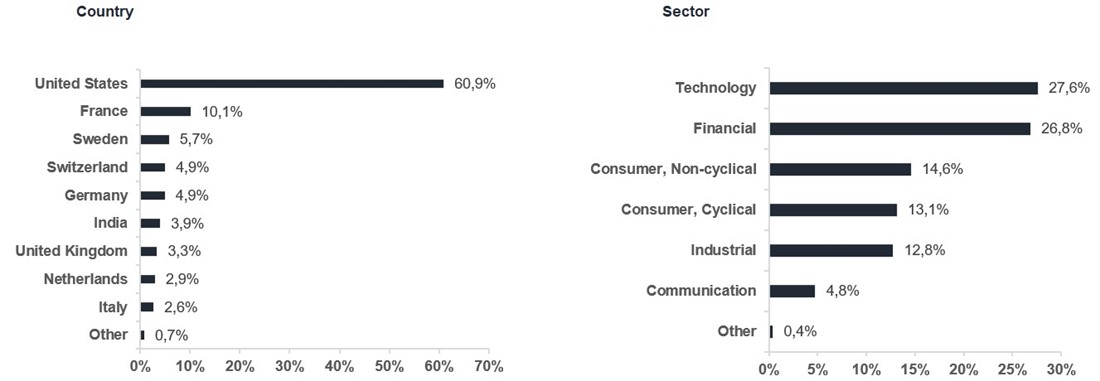

According to Chinese astrology, 2025 is the year of the snake, a time for transformation (think: shedding the skin) and we find it hard to see a more fitting phrase than this to describe what is going on right now. The world is changing, and so is our fund, as we increase our weighting in Europe and reduce the share in the US.

Both political opinions and real-life events affected the stock markets during the month and, although the underlying sentiment has been negative, there are also many companies that will benefit as the playing field is redrawn. Some general observations from our many company visits in recent weeks:

In the fund now, we are laying much of our focus on investing in non-US stocks.

Portfolio changes

We have no new changes to holdings to report. During the month, we markedly decreased our weighting in Nike.

The fund's positioning—our market expectations

We have a healthy global portfolio of what we consider to be the world's finest companies, our Champions, in sectors like industrials, retail, tech, logistics, construction materials, and insurance. We also have our exciting collection of Special Situations, which we invest in at relatively low valuations and aim to sell at higher values. Our investment in Veolia is a prime example of a stock in which we anticipate significant upside in the next 12–18 months.

*MSCI All Country World NTR $ in EUR

| 1 mth | YTD | 5 years | Since inception | |

| BMC Global Select - R EUR | -5,96% | -6,89% | 99,68% | 184,71% |

| Benchmark | -7,64% | -5,55% | 105,66% | 167,06% |

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

Progressive Corporation

HCA Healthcare

Veolia

MICROSOFT CORP

S&P GLOBAL

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 apr 2025

Monthly Newsletter | 8 apr 2025

Monthly Newsletter | 8 apr 2025