We manage our funds according to the principles of sustainable investment (ESG: Environment, Social, and Governance). We strive to invest our unitholders' capital in companies that recognize the importance of ESG and have incorporated these principles into our investment process. We do this because we want to. The world faces numerous challenges, and we want to be part of the process in helping to resolve these. It is essential for us that a company has a sustainable business model that incorporates ESG.

We also believe that companies taking ESG seriously are better run than others and create higher potential returns for our unitholders at lower risk to their investments.

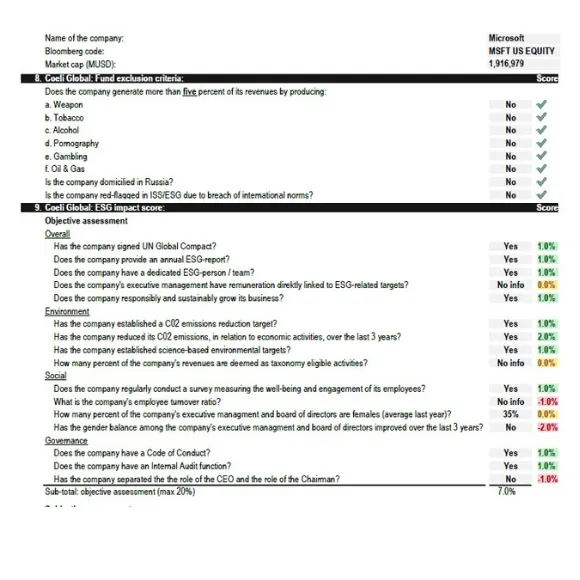

We exclude

Before we make an investment, we always conduct ESG exclusion screening and analysis, through which we exclude companies with more than 5% of their revenues from the production of fossil fuels, tobacco, alcohol, pornography, weapons, or gambling. Note: gambling (betting) rather than gaming (computer gaming). We also exclude companies that fail to respect the international agreements and norms on human rights, working conditions, environmental issues, and anti-corruption. We use the analysis tools from independent provider MSCI ESG at this stage.

Why do we set a 5% cut-off? This cut-off is often used when fund management firms talk about which investments they will exclude, and it is also in accordance with the Swedish Investment Fund Association's "Guidelines for marketing and information by fund management companies." Situations could occur such as a global industrial corporation with a small proportion of its business in some countries that sell military defense equipment, for example, or that a by-product from its industrial process can be considered a fossil fuel. Our intention is to not invest in companies involved in the areas stated above, but it can also be challenging to anticipate exactly which of these scenarios could occur, and so we have also decided to use the 5% cut-off.

We select

All else being equal, we prefer to invest in companies that take ESG issues seriously and whose businesses have a positive environmental and social impact. In our experience, such companies are often not just well run but also prove to be investments that offer high returns to our unitholders. Our analysis "out in the field" meeting leading scientists is a key part of our work when searching for companies, while our desk-bound work involves looking through those companies highlighted as good ESG performers by other institutions, subsequently establishing contact with them and undertaking our own analysis.

We analyze

When we have found an interesting company, we begin our own analysis. Before investing, we undertake the exclusion process outlined above. After that, we scrutinize the company's ESG profile, investigating its ESG reporting, climate initiatives, social impact, and corporate governance, focusing on its internal accounting and shareholder program. Through this analysis, we assess how large the company's environmental impact is versus the size of its business. We also evaluate the company's ESG risks and opportunities.

The asset managers quantify the company's ESG profile and include this in the valuation of the company. For companies that we judge as taking ESG seriously, that conduct measurable climate initiatives, and that are well run, we assign a valuation premium compared with comparable companies that fall short on these attributes. We anticipate higher upside in equities with such a premium and so we are more likely not only to invest in them but also to keep them in the portfolio for a longer time than those without this valuation premium.

– ESG also forms part of our evaluation of a company's business model and our ongoing risk analysis.

We influence

We influence the companies that we define as Champions via an Impact Letter, in which we outline our expectations as a shareholder. For example, we urge them to sign the UN Global Compact—the UN's international principles regarding human rights, working conditions, environmental issues, and anti-corruption directed at companies. In our discussions with companies, we promote #5 of the UN's Sustainable Development Goals (Gender Equality) and #13 (Climate Action) by encouraging the companies to work actively with these vital issues.

In addition to this letter, ESG issues form a recurrent theme in our meetings with company representatives, regardless of whether we own shares in the company or not. In a typical year, we conduct over 100 interactions with different companies around the globe.

Our ESG work is under continuous development. By refining our processes as we learn more, we not only have a greater influence on our holdings but can also generate higher returns at a lower risk. ESG is not only gratifying but also important and valuable to our unitholders. We are thankful for our unitholders’ faith in us in this work.