Herman Ohlsson

Analyst with a focus on the semiconductor industry, Brock Milton Capital AB

In this blog post, I will look at how Taiwan has succeeded in becoming the key player in the semiconductor industry and share some of my insights from my analyst visits there. In May earlier this year, I traveled to Taiwan to visit several of the country’s semiconductor companies, to understand the ecosystem around the industry and get a feeling for the geopolitical threats from the other side of the Taiwan Strait. I headed 80km south of Taipei to visit the city of Hsinchu, the heart of the semiconductor industry. But first, let’s take a look at some history.

Morris Chang and the founding of TSMC—putting Taiwan on the world map

To understand why Taiwan has become so dominant in the manufacturing of semiconductors, we need to head back to 1987 and the founding of TSMC (Taiwan Semiconductor Manufacturing Company). The company was established by Morris Chang, a Chinese man who emigrated to the US in his youth and later studied at MIT, Stanford, and Harvard. He subsequently spent several years at Texas Instruments before moving to Taiwan and founding TSMC with the help of the Taiwanese state. It was the starting gun for what is today’s the world’s largest semiconductor manufacturer and among the most important companies for technological development. Today, 60% of the world’s semiconductors are manufactured in Taiwan and 90% of the most advanced are used in smartphones, data centers, and to train AI models.

The key reason for the establishment of TSMC was that a new form of business model had sprung up in the semiconductor industry. From its creation in the 1950s and up to the early 1980s, the industry had been dominated by companies that designed and manufactured semiconductors.

But as production costs shot up and companies saw sizable fluctuations in demand, a new type of company stepped up: the foundries. TSMC was the first, after Morris Chang came upon the idea solely to manufacture semiconductors for other companies, and thus offset these large demand swings by producing for multiple different companies and their products.

This also resulted in the emergence of the “fabless” business model, where companies like Nvidia and AMD could allocate their entire focus on design, without having their own factories (fabs), instead letting TSMC handle the manufacturing for them. In this way, TSMC lowered the entry barriers for companies to start designing semiconductors with the need for their own manufacturing. This model is today the industry standard, with a new semiconductor factory costing around SEK 200bn to construct—70% of the costs go to equipping the factory with expensive production machinery. A single semiconductor machine from the Netherlands’ ASML costs close to SEK 2bn, and each factory requires a dozen or so. Entry barriers to start competing with TSMC can thus be said to be particularly high. This has, alongside a tireless focus on innovation in an industry that has outsourced its production, paved the way for TSMC’s success that put Taiwan on the map.

It was no coincidence that Morris Chang got the opportunity to start TSMC in Taiwan. The Taiwanese state had recognized that the US’s heavy dependence on it also protected it from the growing threat of China. Co-operation between them is today considerable, and several US semiconductor companies—such as Cadence, Synopsys, Texas Instruments, Applied Materials, and LAM research—are represented on Taiwanese soil. A visit to Hsinchu soon reveals that all the semiconductor companies are represented in the city in order to allow for closer collaboration between customers and suppliers. For example, all equipment suppliers (ASML, ASM, Applied Materials, etc) have offices in Hsinchu to co-operate closely with their largest customer, TSMC, which annually purchases semiconductor equipment for around SEK 250bn.

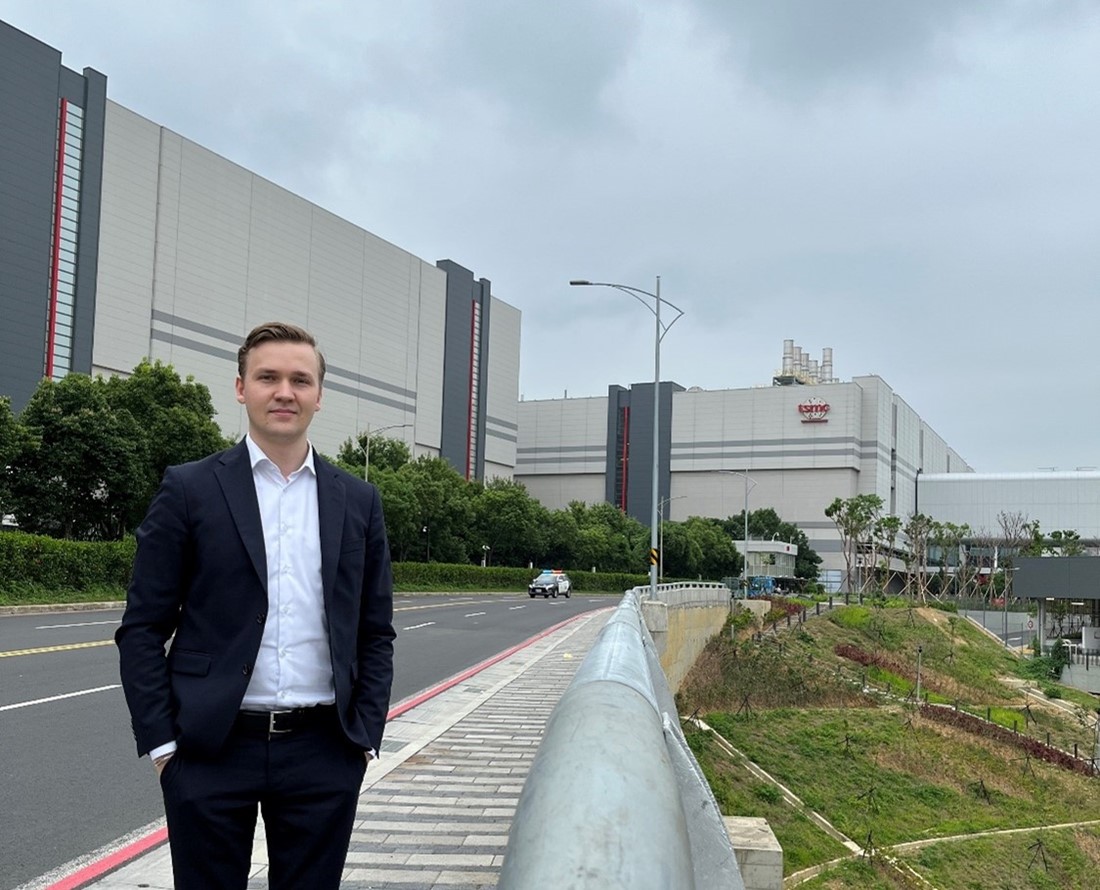

Outside one of TSMC’s factories in Hsinchu earlier this year. The city is home to around twenty factories, each one larger than a soccer stadium.

Outside one of TSMC’s factories in Hsinchu earlier this year. The city is home to around twenty factories, each one larger than a soccer stadium.

Semiconductor industry built on global co-operation

It is not just the US and Taiwan that collaborate in the global semiconductor value chain. During my visit, I learned just how integrated this value chain is. A shuttle service of trucks operates between the factories in Hsinchu, delivering gases, chemicals, and machinery to maintain the smooth running of production around the clock. Machinery is delivered from the US and Europe, gases from China, design software from the US, and chemicals and silicon wafers from Japan. We can say that nowhere in the world is close to being self-sufficient in semiconductors but that the industry relies on close co-operation between countries and companies. As no country can do everything from start to finish, the value chain is based on an ecosystem built up over a long time that today offers economies of scale and lower costs. Production has centralized in Taiwan as it is around 30% cheaper to construct a factory there compared to in the US.

Likewise, companies like AMD and Nvidia are based in Silicon Valley because that is the center of excellence for the best design engineers. This means that the value chain is particularly vulnerable—something we saw during the Covid-19 pandemic, when deliveries of materials and equipment were delayed. At the same time, demand rose sharply as people were suddenly forced to work from home and equip their home offices. Considering the high costs involved in constructing a factory (SEK 200bn) and designing a semiconductor (SEK 5bn), the value chain has thus consolidated to a few companies with almost uniquely rock-solid market positions. A couple of examples: ASML holds a 100% market share in EUV machines, Nvidia has a 90% share in AI chips, ASM has a 55% market share in machines for deposition, and the market for design software is a duopoly controlled by Cadence and Synopsys. The world is not only particularly dependent on Taiwan for manufacturing but also on only a handful of companies in the entire industry. This has meant splendid margins, solid growth, and high entry barriers with limited risk of competition. A consolidated market has also led to semiconductor companies seeing especially good pricing power—i.e., the possibility of raising prices for customers. A key reason is also that semiconductors are the brains in all today’s electronics and are thus a driving force behind technological development.

Reshoring is the result of the pandemic

A functioning supply chain of semiconductors is required for this technological development to continue. The Covid-19 pandemic and the higher costs it brought with it for many companies when they couldn’t access the small key components needed for their production has prompted a global reshoring trend, not just in semiconductors but generally speaking. Companies have moved parts of their production—mostly from China—to diversify their supply chain and reduce the risk of future issues. We see a particularly convincing trend in the US, but also in Europe, where much semiconductor production is being moved. TSMC alone has announced two factories in Arizona totaling SEK 400bn, due for completion in 2025 and 2026. A staggering sum that certainly benefits equipment producers as more factories are equipped with increasingly advanced machines for semiconductor manufacture.

The geographical diversification of semiconductor production will likely prove tougher than many thought. To build a factory is one thing, but to move and re-establish the ecosystem that exists around the Taiwanese factories will take time. The world will be able to produce semiconductors in several regions, but it is likely to long remain dependent on a few suppliers in the value chain.

This global diversification of semiconductor manufacturing will come at a cost over time. The threat of China invading Taiwan will increase as the world becomes less dependent on it. It is thus in Taiwan’s interest to remain the hub for the world’s semiconductor production to reduce the incentives for any possible aggression.

Taiwan is China’s largest trading partner

China has long tried to make itself self-sufficient in semiconductors—without success. Today, only 15% of the world’s semiconductors are made in the country, despite massive economic and political initiatives. Given the current dependence on Taiwan, Chinese aggression against it would devastate the digital economy, impacting China itself as well. The country’s largest importer and trading partner is in fact Taiwan. China is also by far the world’s largest importer of semiconductors, purchasing USD 170bn worth of semiconductors each year. The reason for this is that a majority of final assembly occurs in China. However, final assembly is a simpler stage in the value chain, mainly requiring a large scale and a cheap labor force, both of which are found in China. As part of the reshoring trend, much final assembly is moving to South East Asian countries, as attested to by several of the companies I met in Taiwan. China thus lacks leverage in the global semiconductor industry and is itself dependent—to say the least—on Taiwan’s semiconductor factories running at full speed around the clock.

Sources: Trading Economics, Worldstopexports.com, General Administration of Customs of the People’s Republic of China, OEC, Semiconductor Industry Association (SIA), Coeli Global

Analyst with a focus on the semiconductor industry, Brock Milton Capital AB

Blog | 12 mar 2025

Blog | 24 maj 2024

Blog | 15 mar 2024